Often, I hear people say that they hate car shopping. It’s a process and it takes some time. You don’t buy a house in a couple of

hours. Buying a car takes time, but you

can help the process along by going to your dealership prepared. By bringing the following documents along,

you can help us get you on the road in your new vehicle even quicker.

Your driver’s license:

Sounds like a no brainer, but you must have a valid driver’s license to

take a test drive. Also, your driver’s

license is your valid form of identification.

Trade title: If you have a

trade vehicle, you should bring in its title.

If the vehicle has no lien, then you should have this important

paper. It often gets misplaced, so if

you are thinking about car shopping, you should be locating this paper or

getting a replacement if you can’t find it.

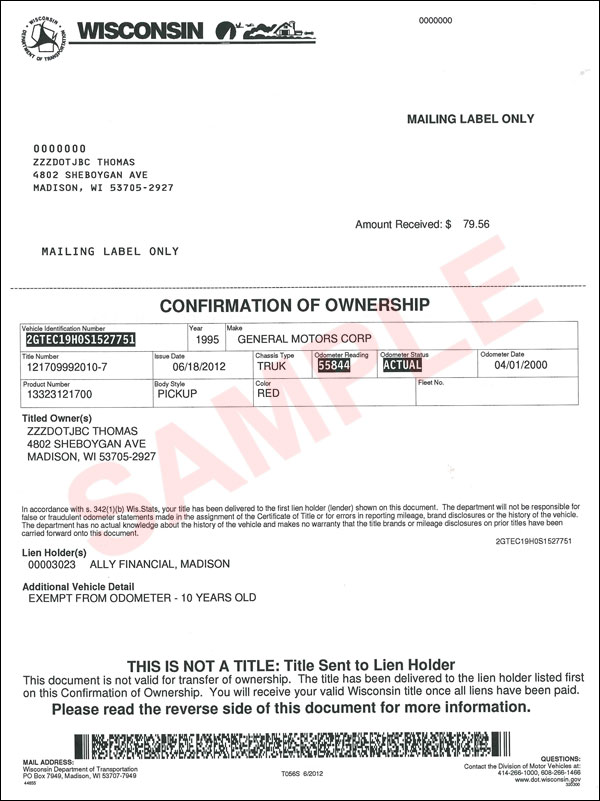

If there is a still a loan for the vehicle, the bank may have the title

in their possession. In Wisconsin, the

titles are now held by the bank until the loan is satisfied.

Starting July 30, 2012, Wisconsin Division of Motor

Vehicles (DMV) began delivering titles to lien holders consistent with recent

statute changes. Any title with a lien (loan) listed on or after July 30, 2012

is sent to the lien holder. Lien holders may receive titles in a paper or

electronic format. Owners of vehicles receive a Confirmation of

Ownership and will receive the actual title when all liens are

paid off.

{kind=link}

Note that if you already have your title (even if it

lists a lien holder), nothing changes. You can keep it. Titles will only be

issued to lien holders on or after July 30, 2012. (reprinted from Wisconsin DMV Website; for

more info http://wisconsindot.gov/Pages/dmv/vehicles/title-plates/lienholder-default.asp )

Proof of insurance: If you

are financing your new vehicle, you must provide a copy of your insurance card

with full coverage. If you are pondering

leasing a vehicle, you may be required to have a little higher level of

insurance. Before you begin car

shopping, it might be a good idea to contact your insurance agent and increase

your levels of coverage if they will not meet your needs.

Proof of income: If you know

your credit isn’t the best or you just started a new job within the last year,

the financing department may require you to show proof of employment by bringing

them your latest pay stubs. You may be

asked to provide proof of income for other forms of income, like child support,

if it is being used as consideration for a loan.

Proof of residency: If you

have recently moved and your current address does not match your driver’s

license, you may be asked to provide proof of residency. Usually some sort of utility bill or a

recurring bill to your new address will suffice.

All deciding people present:

This may seem like a no brainer, but quite often, people come shopping

and not all parties are present. A

co-signer may be absent, husband or wife, mother or father. Not having all people available slows down

the process considerably.

If our customers come prepared, the process moves along at a

much smoother pace. Everyone’s situation

is different, but doing a little preparation ahead of time will save you some

valuable time.

No comments:

Post a Comment